Jul 31, 2024

Jul 31, 2024

Note: This article was updated on February 2026.

Automatic bank reconciliation, a global market predicted to reach a value of nearly €5.5B by 2032, significantly enhances the products offered by accounting and financial software providers. But to tap into that market and become a real-time source of financial data, you must build or buy a reliable automated reconciliation system that delivers the bank coverage and connectivity your customers demand.

What “automated bank reconciliation” actually means

Bank reconciliation compares a business’s or an individual’s financial records (such as deposits, withdrawals, and checks) with the corresponding bank statements to validate the former’s accuracy. The reconciliation process must address the records of both accounts payable and accounts receivable (in this article, we focus only on automating reconciliation for accounts payable).

Automated bank reconciliation simply means that the process is handled automatically using Open Banking, embedded payment technologies, other API-based technologies, or a combination of the three. An automated solution can detect errors, prevent fraud, and help to maintain accurate financial records, all without requiring manual intervention.

France today: the 4 key foundations that enable full reconciliation automation and how to set them up

Your first step in rolling out automatic bank reconciliation is to set up the necessary foundations to access the relevant data. These can be broadly categorized into four groups:

- Open Banking connectivity for bank accounts.

- Payment provider connectivity for PSP wallets.

- Invoicing connectivity for sales and supplier invoices.

- Embedded tracked payment for transaction reconciliation.

The next sections detail financial software providers’ options for integrating each connector and payment feature.

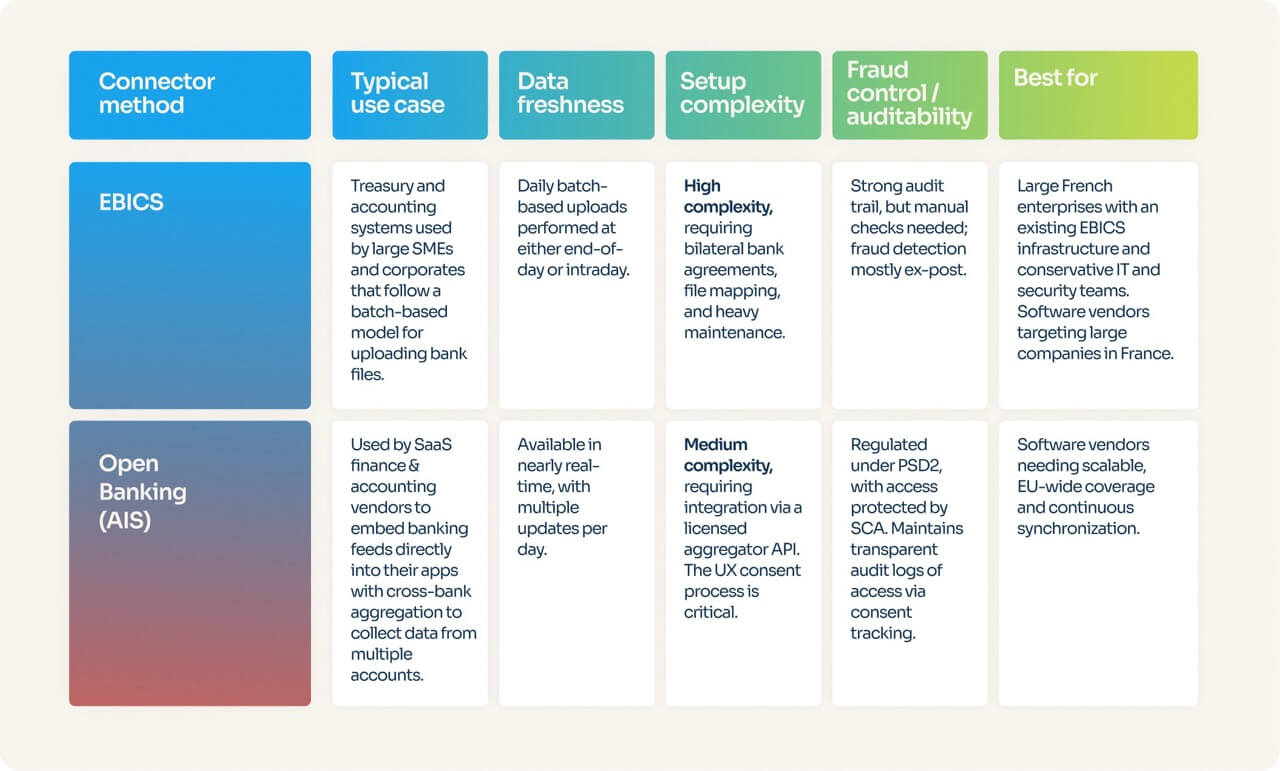

Establishing bank connectivity in France: EBICS vs. Open Banking

In France, the two most common methods of establishing banking connectivity for automated reconciliation are EBICS and Open Banking.

EBICS

The Electronic Banking Internet Communication Standard (EBICS) is a widespread communication standard between European banks and corporate businesses.

Despite its necessity and widespread usage at the corporate level, EBICS remains the least technologically advanced method and also the most expensive. It operates on a file exchange, batch-based model, limiting real-time transaction processing capabilities, and also requires heavy setup. While it’s a stable option for large companies, EBICS can be ill-suited to SaaS software targeting freelance and small companies that want to scale quickly within Europe.

Open Banking (AIS) aggregation

Bank reconciliation via Open Banking involves direct connection to banks via APIs. For example, AIS (“Account Information Service”, the regulatory name of Open Banking) under PSD2 allows Powens to fetch standardized account data across banks, all through an API. Unlike the batch-based EBICS files, AIS can deliver near real-time feeds of data at multiple points in the day. Compliance is built in through a standardized user consent process. Access to data is protected by Strong Customer Authentication (SCA) protocols that dictate that users must be authorized via two factors out of the following three: something you know (e.g., a password or PIN), have (e.g., a phone), and/or are (e.g. fingerprint or a biometric sign).

The catch comes in the user experience. SCA consents expire every 180 days, so if you have a poor UX design for managing consent renewals, you’re likely to witness significant drop-offs (which is why Powens’ solution for bank aggregation already comes with a best-in-class consent UI).

Avoiding the SCA consent pitfalls requires a strong aggregator that can smooth bank API inconsistencies while simultaneously maximizing conversions.

Most financial software vendors begin their reconciliation automation journey with AIS for three reasons:

- Faster integration via a single API instead of EBICS’ bilateral bank agreements and individual connection management.

- Scalable coverage across the EU from day one

- Sufficient for most reconciliation needs, with the option to add IBANs and PSP/document enrichment later on for full automation.

Setting up payment provider (PSP) connectivity: build vs. buy

In addition to connecting bank accounts, you can also connect payment service providers (PSPs) to your system when a significant part of your customer base sells online. This can include both global players, like PayPal, Stripe, and Adyen, as well as local providers, such as PayPlug and CentralPay.

You have two options for setting up these connectors:

In-house development

Since most PSPs offer public APIs, in-house development is an option. It offers you greater control over your financial infrastructure, but comes at a higher cost and complexity. Project timelines for developing PSP connectors can vary from a few months to a year or more, especially when it comes to mapping data objects that can differ widely between providers.

Extended Open Banking providers

Extended Open Banking providers can offer faster rollout timelines by integrating an existing, compliant solution that requires minimal capital expenditures and increases operational expense flexibility.

Powens, for instance, provides connectivity to both PSPs and banks, giving you a bundled solution that streamlines your connector integration process.

Adding invoicing connectivity

In cases where your B2B customers do not use your software to issue sales invoices, bank reconciliation can remain a pain: you need invoice data to match with your bank transactions. Research on omnichannel embedded accounting shows that 78% of reconciliation errors occur due to data silos between sales channels and accounting systems, while automated synchronization between these channels and systems can reduce manual reconciliation efforts by up to 92%. Obviously, similar issues arise with supplier invoices.

In such cases, accounting software can opt to connect directly to the software or platform that issued the sales invoice or the supplier invoice. We’re talking connectivity to CRMs, invoicing tools, POS, and also spend management software.

Before we go through the options to set up this kind of connectivity, a word on e-invoicing. If e-invoicing is already in place in the countries you operate, you probably have to connect to a regulated e-invoicing platform (whether public or private). This way, each sales invoice issued via your software will go through a routing mechanism that will automatically send the invoice to the customer. And since we’re talking about structured digital information, it will be easy to automate reconciliation. But note that e-invoicing alone won’t give you 100% automation. A customer might operate (and issue invoices in) multiple countries, including countries where e-invoicing is not in place; also, a customer that is operating 100% in a single country might receive supplier invoices from foreign providers that are not subject to e-invoicing mandates – so those supplier invoices won’t be collected automatically.

In short, because e-invoicing is not mandatory in all countries, it cannot, on its own, deliver full automation of sales invoice reconciliation across all geographies.

So, if you’re considering deploying invoicing connectivity, you have two options for setup:

In-house development

Again, developing invoicing connectivity in-house allows you to tailor the connector to your needs, but it can eat away at your budget if you are not a large corporate entity. You must commit substantial resources and prepare to allocate significant business time to ongoing maintenance.

Specialized API integration software

Invoice connectivity is incredibly important for accounting software providers to achieve full automation. In fact, so much so that accounting software provider Pennylane acquired the invoice connector Billy in 2024.

If you’re looking to rent instead, specialized API integration software, such as Chift and Paragon, are ready-made solutions for retrieving invoices. Some providers even offer connections to most of the major CRMs and POS, normalizing the data model of all the respective APIs within a single solution.

Rolling out embedded tracked payment

Embedded tracked payments allow financial software providers to offer payment methods that can automatically reconcile invoices with transactions and clarify the payment’s source.

Property management companies are a good example, as they need the ability to know exactly where a rent or property expense payment came from and which tenant or property it relates to. To gain these capabilities, companies can choose between one of three main solutions:

- Payment Initiation Service (PIS): Also known as pay-by-bank or request-to-pay, PIS means that a licensed third-party provider (TPP) executes a payment via direct bank transfer from a user’s bank account after they give their consent for the transaction. This solution is best for collecting and reconciling low-value, one-off payments, such as an ecommerce transaction. For instance, accounting software could pre-prepare a wire transfer, set up the destination IBAN, label, and establish an ID for that specific payment.

- SDD (SEPA Direct Debit): Ideal for pulling funds and reconciling high-value fixed or variable recurring payments, such as subscriptions or utilities. Unfortunately, SDD payment failures can be expensive at roughly €10 per payment. These costs can be mitigated when SDD is combined with complementary tools – such as Open Banking balance checks – made possible by providers like Powens.

- Virtual IBANs: Virtual IBANs (vIBANs) enable auto-tagging of incoming funds, a capability ideal for receivables, sub accounts, and completing reconciliation at the source. vIBANs are well-suited to companies that deal with a lot of heterogeneous payments from multiple different counterparties, such as rent payments or maintenance fees in property management.

In most cases, payment initiation and SSD are sufficient. vIBANs make the most sense when receiving high volumes of payments from different parties that need to be automatically sorted into the right subaccounts or categories (e.g., rent payments, maintenance fees, etc.).

Powens offers solutions for all three methods detailed above (PIS, SDD, and vIBANs), meaning you can adapt your strategy according to specific scenarios.*

*vIBANs, SDD, and SEPA transfers are provided by Unnax Regulatory Services EDE, S.L. (part of Powens Group) under its electronic money license (Bank of Spain registration code 6719).

Quick start for software providers (how to build this right)

For financial software providers implementing automated bank reconciliation, the architecture blueprint centers on data modeling, mapping, and a comprehensive rules engine.

Beyond establishing the four foundations to pull data, providers must also define how those data points interact. Accuracy is vital for ensuring accounting and banking records match, while automated rules for exceptions and thresholds can maintain a high efficiency rate for handling minor discrepancies. Only significant variances get flagged for manual review.

Tips: what is often underestimated:

- Consent UX is key: Open Banking Consent UX that actually converts and boosts acceptance and renewal rates is short and branded with familiar bank logos. Your consent UX should contain pre-filled hints, retry patterns, and an SCA explanation. Powens’ solutions cover your UX bases with best-in-class UI and acceptance rates up to 75%.

- Fill data gaps with PSP connectors: PSP connectivity to CRMs and other software providers can fill in the missing gaps needed for full reconciliation, such as receipts, invoices, and attachments (from providers like Stripe and PayPal). With Powens, you can retrieve both transactions and related documents from PSPs and neobanks.

- Timelines: Leveraging a ready-made connector or payment solution allows you to achieve a faster time to market for an automatic bank reconciliation rollout, saving significant time compared to building in-house solutions and obtaining the right licences to provide them to your users. Powens enables you to roll out quickly in 3–4 weeks, depending on complexity.

Step-by-step: how to start automating bank reconciliation

- List sources you want to connect to (e.g., banks and neobanks via AIS + PSPs) and define your KPIs.

- Choose the best aggregation solutions for your needs (coverage, features, support). Do not forget to check the providers’ API documentation and evaluate the gap between their data model and yours.

- Implement an AIS aggregation solution, such as Powens, that includes a free sandbox environment and A/B testing for optimizing consent UX design.

- Add PSP and neobank connectivity. Powens includes this.

- Ensure a parallel run to compare against last month’s close to compare mismatch rates and cycle times. Make sure to keep manual banking transaction imports as a fallback mechanism.

- Roll out fully with monitoring dashboards to keep track of automation performance.

What to implement next (maturity path)

Reconciliation automation matures over time, with software vendors starting simple and adding advanced features as volumes, clients, and compliance needs grow. The ideal maturity path can depend on your use case, but should generally follow this flow:

- Implement an AIS integration as your baseline for automated reconciliation.

- Add your PSP and neobank connectors to capture pay-ins, payouts, and attachments.

- Implement an invoicing connector for document enrichment (takes 1 to 2+ months)

- Introduce rule engines, queues, and monitoring for mismatches via an exceptions dashboard.

- Embed payments with payment initiation, SDD, and Virtual IBANs

- Extend automation to your supplier payments, cross-entity treasury, and predictive cash management with payout reconciliation and advanced analytics.

The smartest providers evolve gradually. Reap quick wins with AIS, then roll out enrichment and IBANs later down the road for full automation and adequate fraud prevention.

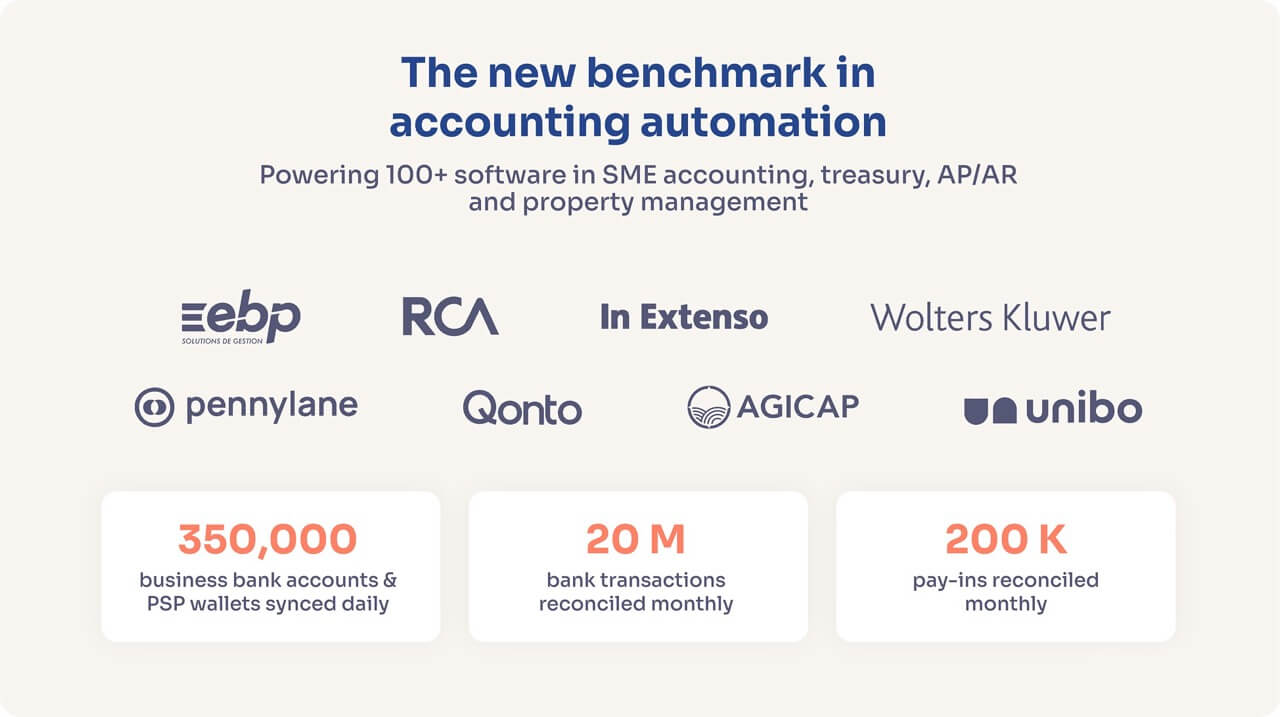

Real-world case studies

Check out how real companies are using Powens’ solutions:

Pennylane

Thanks to Powens, Pennylane synced 120,000 SME accounts with daily data refreshes, enabling it to achieve a stability level ranking two times higher than with other Open Banking providers.

Qonto

Through deploying Powens’ solution in four countries, Qonto achieved pan-EU aggregation and a strong consent UX with an NPS greater than 75. It now operates as a neobank with 600K+ customers, offering embedded accounting capabilities.

👉 Read the full case study with Maxime Champoux, Head of Product at Qonto

Agicap

Agicap leveraged Open Banking with the help of Powens to enable real-time cash tracking across more than 6,000 customers and 11 countries. It has raised €100M since its inception.

👉 Read the full case study with Jérémie Barbet, deputy CPO at Agicap

Buy vs. Build: Two options for automated bank reconciliation

Compliance, security & auditability in France

Your reconciliation flows must align with regulations like PSD2, GDPR, and French audit norms. AIS can both speed up the process and strengthen traceability by meeting the following requirements:

- PSD2 & SCA: Every bank connection requires Strong Customer Authentication (SCA). All access must be explicit, user-consented, and regulator-approved.

- Consent windows: Access renewals every ~90 days. Ensuring good consent UX can minimize drop-offs and provide key support for audit logs and continuity.

- Data minimization (GDPR): Only fetches what’s necessary (such as balances, transactions, and counterparty info). Justify when documents/PSP data are included.

AIS also complements EBICS’ batch files with real-time, per-user consent logs that provide stronger overall evidence to share with auditors and regulators. For software vendors, AIS means faster reconciliation and a stronger compliance story.

Buyer’s checklist for selecting a reconciliation automation partner

Vendors who tick all of the following boxes can help you reduce risk, speed up your time-to-market, and reassure both auditors and end-users:

- Must provide bank coverage for the breadth of French business banks and other EU countries where you have clients.

- Effective consent UX conversion via smooth SCA flows and high acceptance rates.

- Multiple PSP connector options (such as Stripe, PayPal, and SumUp) to achieve full coverage of pay-ins and payouts.

- Embedded payment and payment tracking capabilities to allow for further bank reconciliation automation.

- Document retrieval services for accessing invoices, receipts, and attachments.

- High uptime (ideally >99.9%) and contractual service level agreements (SLAs).

- Integrations with modern treasury and accounting standards to ensure smooth ERP workflows.

- Exception workflows for efficiently flagging, queuing, and resolving mismatches.

- Easy evidence exports of consent logs and reconciliation reports.

- Granular, role-based permissions to control who can access specific information.

Vendors who can tick all these boxes, like Powens, reduce risk, accelerate time-to-market, and reassure both auditors and end-users.

Why Powens is the best choice for automated bank reconciliation

Powens simplifies reconciliation automation with an all-in-one solution built on richer data, reliable connectivity, and tracked payments. As Europe’s Open Finance leader, Powens’ platform uniquely combines broad AIS coverage, enriched PSP data, and Virtual IBANs to help finance and accounting software providers deliver a seamless, automated reconciliation experience to their customers across France and the greater EU region.

Fast facts:

- Reliable AIS aggregation with France and EU-wide coverage (retrieve bank data from ~22 million SMEs across Europe), standardized data feeds, and best-in-class consent UI (75% acceptance rate benchmark).

- Enriched feeds with PSP connectors (Stripe, PayPal, SumUp; retrieve payment data from ~40 million PSP wallets) and document retrieval (receipts, invoices, neobank attachments).

- Virtual IBANs that auto-match receivables at the source, enabling reconciliation at payment level – Powens currently helps reconcile 100M+ bank transactions monthly.

- Strengthened compliance via a PSD2-regulated platform offering GDPR-aligned data minimization and consent logs for auditability.

- Trusted scalability with proven results for clients like Qonto (pan-EU aggregation, NPS > 75) and Agicap (6,000+ customers across 11 countries).

- Quick time-to-market, enabling you to go from sandbox to production in approximately 3–4 weeks with enterprise-grade SLAs.

*IBAN and payment solutions are provided by Unnax Regulatory Services EDE, S.L. under its electronic money license (Bank of Spain registration code 6719).

See Powens’ all-in-one solution in action

Book your demo of our automatic bank reconciliation solution today.