Apr 16, 2026

Apr 16, 2026

In the next five years, Pay by Bank, a type of account-to-account (A2A) payment powered by Open Banking, will become as accessible as card payments. Juniper Research predicts that the number of A2A payment users will grow by 83% between 2025 and 2030. Analysts state this growth will be driven by key advantages like lower transaction fees, a lack of chargebacks, increased security, and enhanced customer satisfaction.

Cards may still hold on to their lead in transaction volume in the near future, but when it comes to the actual movement of money at scale, Pay by Bank transfers are an increasingly dominant pillar of the European payment system.

They also represent a more cost-effective alternative to card schemes, which have historically made up a substantial percentage of the market concentration. Ecommerce Europe reports that card-based payments account for 64% of all electronically initiated payments, and that some large merchants witnessed more than a 75% increase in scheme fees from 2021 to 2026.

As preference for bank-based payments grows, so does the need for solutions designed specifically for this type of transaction. Pay by Bank is one such solution that allows users to authorize a SEPA credit transfer directly within their banking app or online banking portal, without entering card details into the payment interface or leaving the payment environment.

With instant payment regulation accelerating a paradigm shift across the EU and businesses reassessing cost structures, fraud exposure, and operational resilience, Pay by Bank is moving from a niche alternative to a strategically relevant payment method. This signifies a new era for its competitive edge over traditional card payments.

1. What is Pay by Bank?

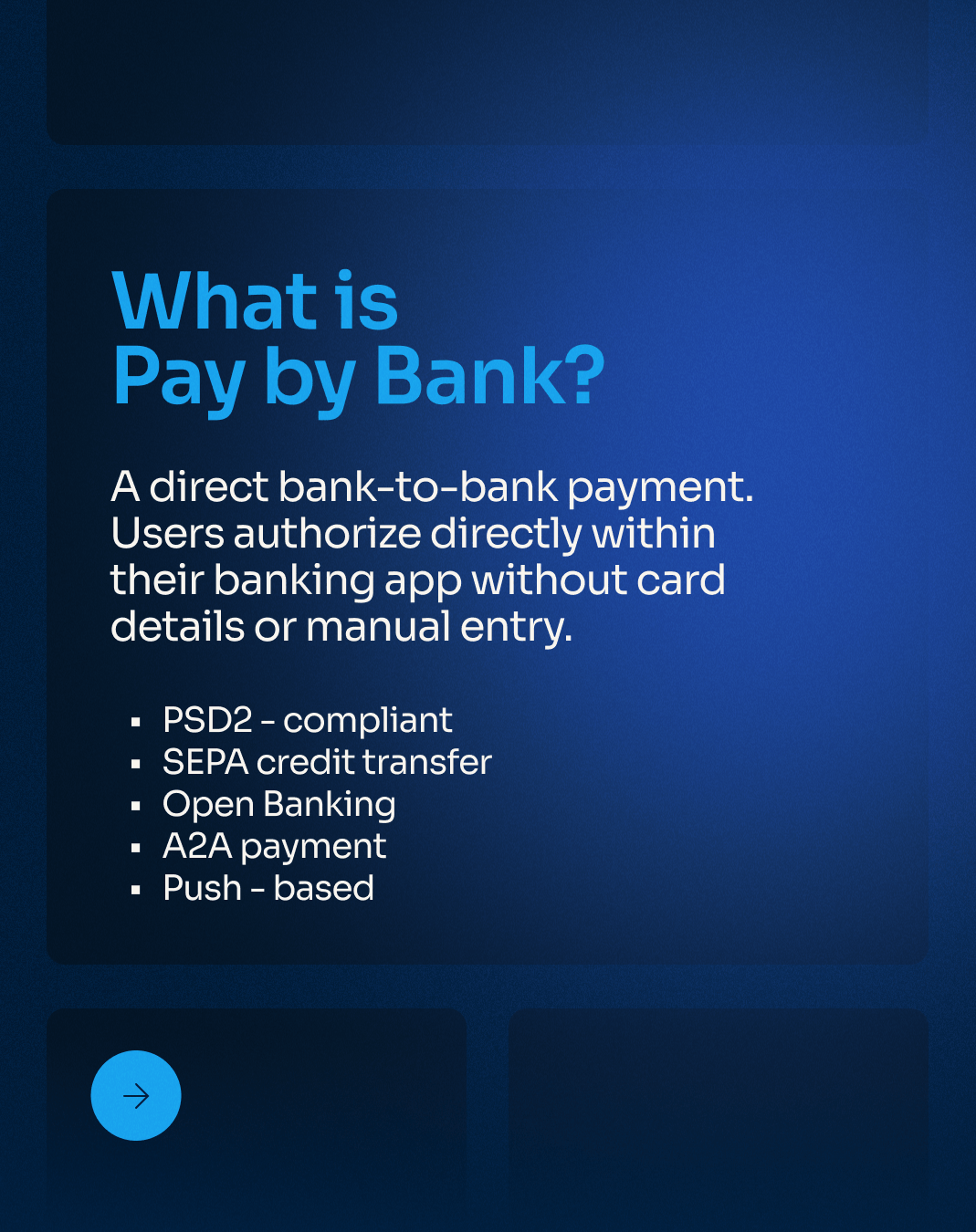

Pay by bank is a Payment Initiation Service (PIS) built on Open Banking that enables businesses to initiate a bank-to-bank payment directly from a customer’s account, with their explicit consent.

Rather than entering card details or using a digital wallet, the customer authorizes the transaction within their own banking environment, typically through their mobile banking app or online banking portal. The payment is then executed as a credit transfer over their bank’s existing infrastructure.

In practice, Pay by Bank can be offered wherever a business needs to collect or send funds, including online checkouts, invoice payments, subscription onboarding, wallet top-ups, or payout processes. For instance, CashSentinel uses Powens’ Pay by Bank solution for car payments within their MyPortal Auto platform.

Regardless of the exact use cases, the principle remains the same: the customer authorizes a direct A2A transfer through their bank.

In checkout use cases, the Pay by Bank option usually appears in the list of available payment methods. It can be stylized in many different ways, such as the following examples below, but will typically read as “Pay by Bank”:

The Pay by Bank method bypasses card networks and enables direct account-to-account payments over bank transfer rails. Because it is built on regulated Open Banking infrastructure, the transfer is initiated through Payment Initiation Services (PIS) with the customer’s consent. In certain use cases, Account Information Services (AIS) can complement this process by enabling real-time balance verification.

2. How does Pay by Bank work?

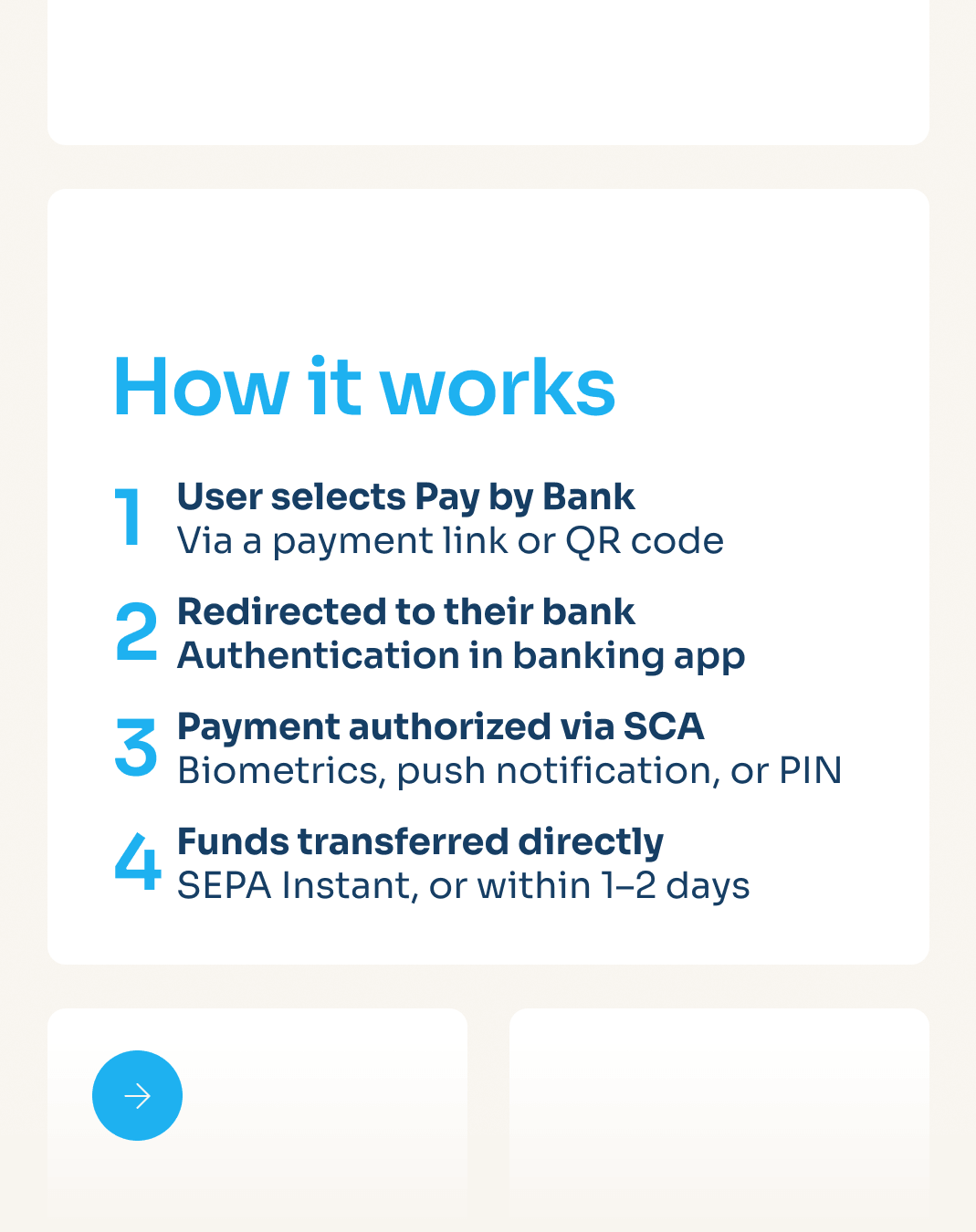

Pay by Bank enables businesses to initiate a bank-to-bank payment within an existing payment flow, whether embedded at checkout, triggered via a payment link or QR code, or used within recurring billing or lending processes.

Once the customer selects the Pay by Bank option, they are redirected to their chosen bank’s online portal or mobile banking app, where the transaction is authenticated using the bank’s Strong Customer Authentication (SCA) procedures. This typically involves biometric approval (e.g., fingerprint or facial recognition) or a secure mobile confirmation, such as approving a push notification or entering a one-time passcode. By completing this step, the customer authorizes the initiation of a credit transfer from their account.

Following authorization, the payment is executed over existing bank transfer rails and sent directly to the business’s bank account. Because the transaction does not rely on card schemes, no card details are entered or stored within the company’s payment system.

After successful authorization, the customer is redirected back to the original payment interface and receives confirmation of the transaction.

The same infrastructure can also support outbound payments (both single and bulk payouts) such as refunds, supplier payouts, or platform disbursements, as well as recurring inbound payments (payins).

3. Is Pay by Bank safe?

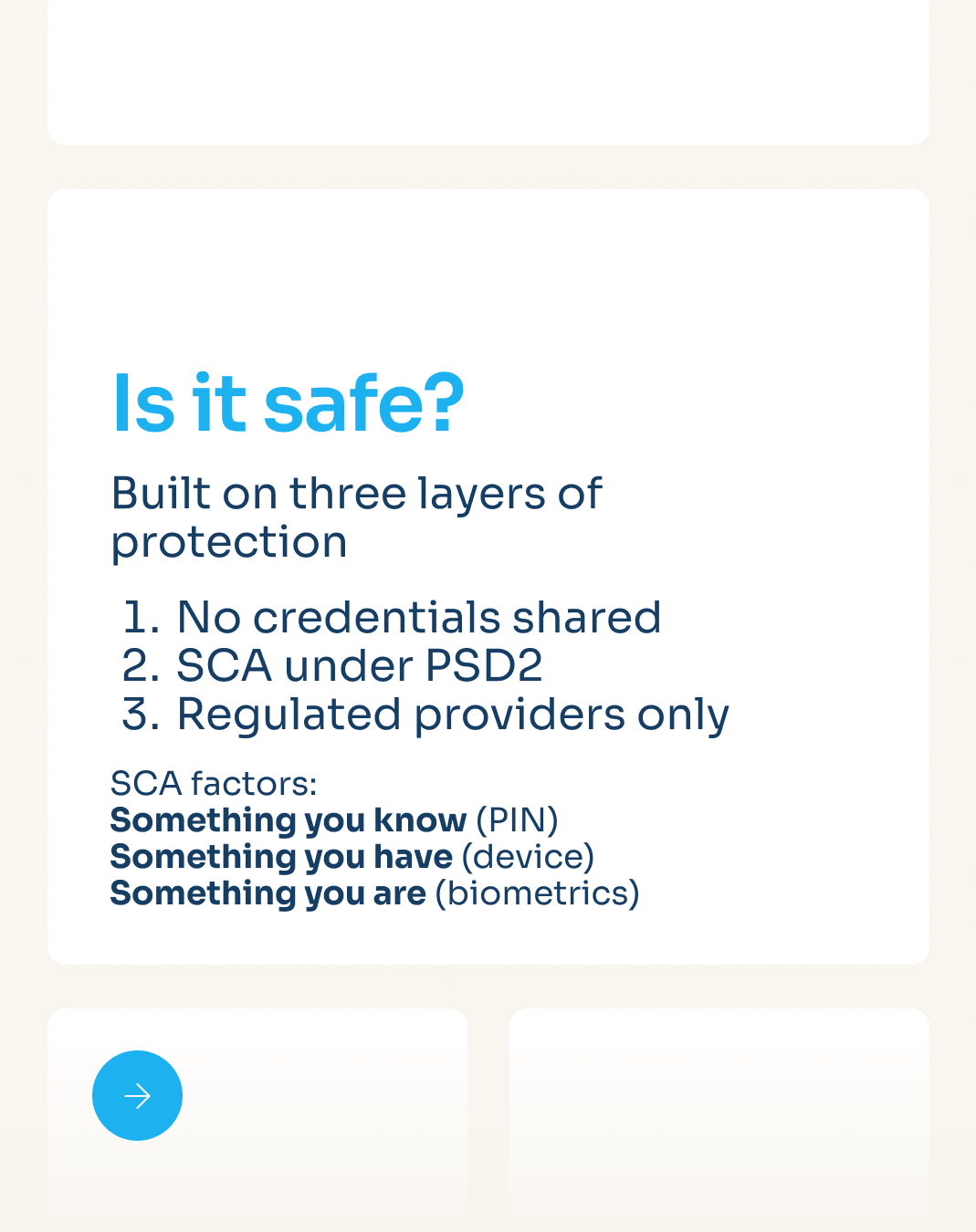

Every Pay by Bank transaction is initiated through a direct, PSD2-compliant API connection to the customer’s bank. The customer approves the payment within their bank’s own app or secure online environment, using their usual authentication methods.

Because authentication takes place entirely within the bank’s infrastructure, the payer’s login credentials are never shared with the business requesting the payment or the payment initiation provider. No card numbers or comparable payment credentials are transmitted to the recipient.

Instead, payment instructions are securely exchanged between the regulated payment initiation provider and the bank via dedicated Open Banking APIs. By eliminating the need to store or circulate sensitive payment credentials, Pay by Bank reduces the amount of exploitable data within the payment chain and limits the overall attack surface compared to card-based transactions.

In addition to this bank-side authentication model, Pay by Bank transactions are protected by SCA under PSD2, which is required for most electronic payments unless a regulatory exemption applies (such as low value, trusted beneficiary, recurring transaction, etc.). SCA requires the payer to verify their identity using at least two independent factors from the following categories:

- Something they know (such as a password or PIN)

- Something they have (such as a registered device)

- Something that is part of what they are (such as biometrics, like a face scan or fingerprint)

These checks are performed within the bank’s secure environment and add an additional regulatory layer of protection against unauthorized access. Transaction details are pre-filled, so customers do not manually enter long account numbers, which limits human error and lowers the risk of being misdirected by scams such as authorized push payment fraud.

Finally, regulated payment initiation providers –– such as Powens, who are authorized to interact with banks’ APIs –– must meet strict licensing, security, and operational requirements under PSD2. They also conduct onboarding and due diligence checks on merchants, helping prevent fraudulent entities from accessing payment initiation services.

4. What are the benefits of Pay by Bank for businesses?

Businesses across multiple industries can benefit from Pay by Bank through a more streamlined and cost-efficient payment flow. It allows for direct connectivity between the payment provider and banking infrastructure.

Key benefits include:

- Familiar UX: Customers can complete transactions in just a few steps without manually entering card numbers in a banking environment they recognize. Once a customer authorizes Pay by Bank, you can initiate transactions on their behalf, including for recurring payments and bills.

- Bank-level security: Approval occurs within the customer’s trusted banking environment, and transactions are authorized using the bank’s own authentication procedures. This reduces fraud exposure and shifts authentication responsibility away from your internal systems.

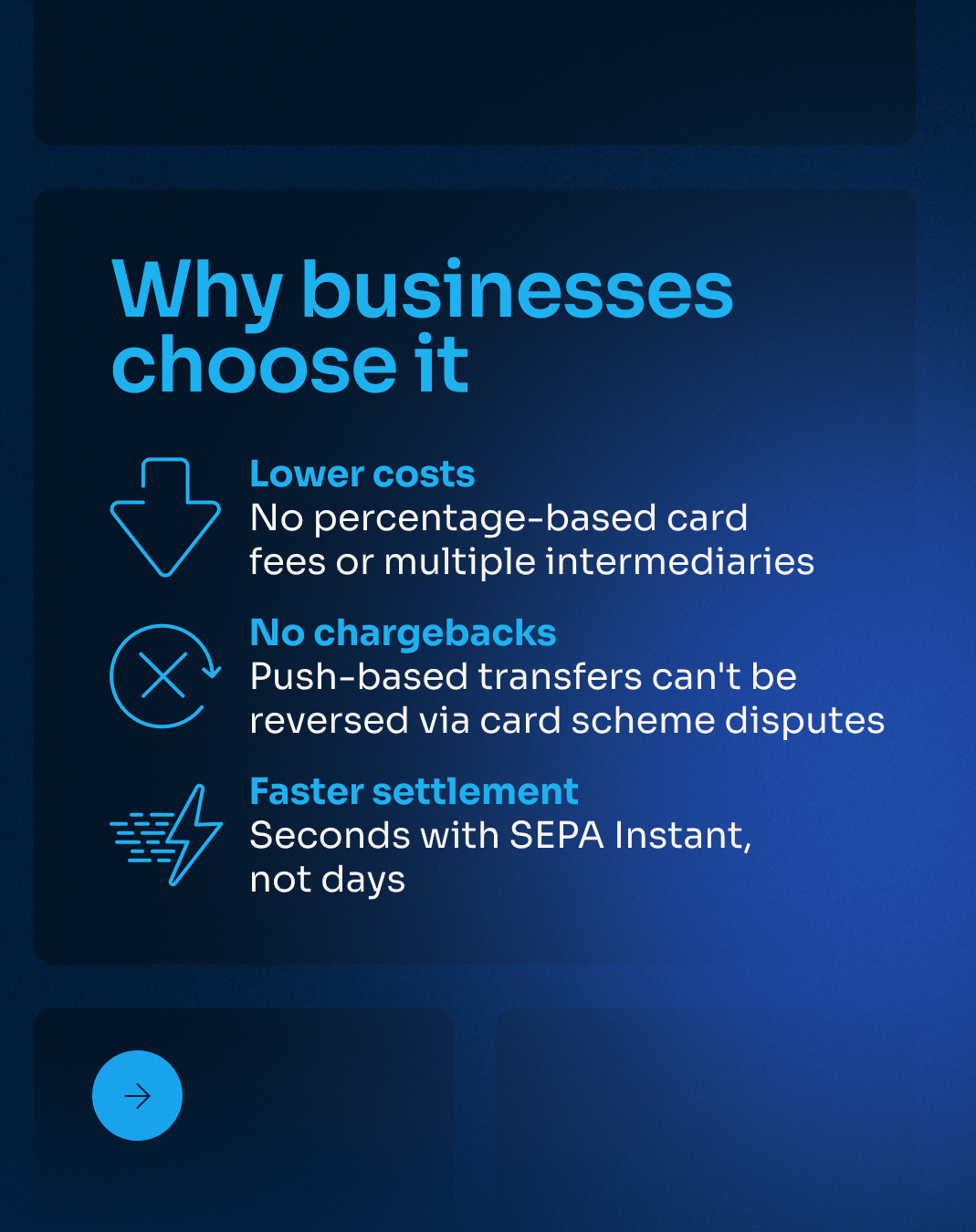

- Faster payments: Funds sent via Pay by Bank are received quickly and are irrevocable. Standard bank transfers within schemes such as SEPA are typically settled within one to two business days, while instant transfers move funds within just a few seconds or minutes.

- Lower costs: Payment processing costs are often lower compared to traditional card payments. Eliminating multiple intermediaries also lets you avoid percentage-based or usage-based fees. Fewer parties in the payment flow can also translate into lower processing and operating expenses.

- No chargebacks: Pay by Bank transactions are executed as push-based credit transfers and do not rely on card scheme dispute mechanisms. Once the customer authorizes a transaction through their bank, funds are transferred directly and are not subject to automated chargeback reversals. As a result, you can lower dispute management costs and prevent costly chargeback-related penalties.

- Improved and automated reconciliation: You can include structured payment references into Pay by Bank transactions, which enables automated matching between bank transactions and invoices. This leads to decreased manual reconciliation needs and improves accounting efficiency.

5. Guide to Pay by Bank use cases across different industries

Certain industries and business models are particularly well-suited to Pay by Bank, such as:

ERPs and financial and accounting software providers

Accounting and financial software platforms and ERPs can leverage Pay by Bank to provide more value to their customer base.

By directly embedding Payment Initiation Services into accounting and invoicing workflows, these platforms can further enhance their existing automation and streamline payment orchestration within a single environment.

This integration allows their users to trigger both individual and high-volume bulk payouts directly from approved invoices, while also supporting payment collection flows (accounts receivable) tied to sales invoices. Using strong authentication protocols and predefined references, Pay by Bank helps streamline both supplier payments and incoming receivables. In invoice-driven B2B environments in particular, PIS-enabled Pay by Bank can achieve high conversion rates, as payments are directly linked to confirmed sales invoices.

When combined with AIS, Pay by Bank allows ERP, financial, and accounting software providers to offer automated reconciliation for accounts receivable as a high-value capability to their users. Payment confirmations and transaction data can be retrieved in near-real time and automatically matched with incoming payments against issued sales invoices within the same workflow. As a result, manual reconciliation steps are eliminated, improving matching accuracy and providing immediate visibility into receivables and payment status. By embedding this functionality, software providers can deliver greater efficiency and financial transparency in AR processes, an increasingly valuable advantage as e-invoicing and digital reporting requirements expand across EU markets such as France and Spain.

Together, these capabilities allow ERP, accounting, and financial software platforms to embed payments and reconciliation directly into their financial workflows, strengthening their role as central infrastructure for managing business payments.

👉 Read more about how financial software providers can automate reconciliation

High-value, one-off payments

Ecommerce merchants can offer Pay by Bank as a secure and more cost-effective alternative to cards for high-value, one-time purchases. Think high-priced electronics or furniture, travel expenditures, tickets, and automotive deposits. Pay by Bank can also be useful as a payment method in environments where large sums are the norm, such as B2B marketplaces, healthcare, or private education tuition payments.

What makes Pay by Bank ideal in these use cases is the lower processing costs compared to the percentage-based card fees that come with traditional card payments. Additionally, since Pay by Bank credit transfers are push-based, merchants and other payees are not at risk of chargebacks. SCA is handled by the bank, keeping the transactions highly secure, and the payee can even enjoy instant settlement times if SEPA Instant is enabled.

With SEPA Instant, funds can be received in near-real time, providing immediate liquidity to the merchant. This contrasts with card payments, where settlement can take several days, and merchants often fulfill orders before actually receiving payment funds. Pay by Bank eliminates this gap between payment and settlement. SEPA Instant credit transfers also typically support higher spending limits than card payments, making Pay by Bank particularly well-suited for high-value payments where cards may fail due to spending limits.

Wealth management and investment platforms top-ups

For wealth management and investment platforms, Pay By Bank plays a crucial part in allowing users to fund their accounts instantly when market opportunities arise. Investors often need to top up their wallets in real-time to execute time-sensitive trades, and any delay in funding can mean missed opportunities. Pay by Bank, combined with SEPA Instant, enables funds to be transferred and made available within seconds, allowing for immediate action. Users can complete fast and frictionless top-ups directly from their native banking environment, which in turn supports higher transaction values and reduced payment failures.

When combined with processing costs that are lower than card payments and comparable to traditional bank transfers, these benefits make Pay by Bank a strong choice for wealth management and investment platforms.

Invoice-based and recurring ecosystems

In industries such as property management, utilities, SaaS, and insurance, payments are typically structured around contracts, invoices, and recurring billing cycles. Here, for fully automated recurring billing, schemes such as SEPA Direct Debit (SDD) remain the preferred method. They enable merchants to pull funds automatically without requiring customer action at each billing cycle. However, Pay by Bank remains relevant in two key use cases: being a complement payment method for both one-off and recurring transactions, as well as facilitating automated reconciliation.

Pay by Bank as a complement to SDD

While Pay by Bank is not designed to replace SDD, it does add a lot of value as a complement at key points in the payment lifecycle:

- Initial onboarding and first payment

- Security deposit collection

- One-off and recurring charges/service fees

- Failed SDD recovery

- Outstanding invoice settlement

For example, property managers may use SDD to receive monthly rent payments, while relying on Pay by Bank to collect a deposit, charge for maintenance, or recover unpaid rent following a failed debit attempt.

Improved and automated reconciliation

Because Pay by Bank transactions are push-based and reference-driven, they are particularly well-suited to invoice-linked payments to improve reconciliation. Each Pay by Bank payment request can include a structured reference (such as an invoice ID or contract number) to ensure that when funds arrive, they can be automatically matched to the correct account, which facilitates reconciliation.

For instance, in property management use cases, tenant-specific references can be integrated into payment links or QR codes for deposit requests, maintenance invoices, and rent collection. Once the transfer is executed, the structured data allows incoming funds to be automatically matched to the right tenant, lease, or property account, reducing manual allocation work.

Lending

Pay by Bank is well-suited for lending, particularly for repayment flows. Instead of relying on cards, lenders can collect installments through account-to-account credit transfers authorized directly in the borrower’s banking app. Because these payments are push-based and authenticated via SCA, they reduce exposure to stolen credentials and card-related fraud.

When combined with the balance-checking capabilities of AIS, lenders can automate repayment prompts to initiate collection requests when sufficient funds are available. This enables smarter collection timing, thereby reducing failed payments.

For consumer lenders, micro-lenders, and leasing providers, Pay by Bank aligns repayment with the underlying banking infrastructure to make collections more secure, automated, and effective.

When Pay by Bank is not ideal as a payment method

Though Pay by Bank has many excellent uses, it is not the best payment method in every scenario. For example, low-value impulse purchases where the customer wants to receive goods or services quickly (such as ordering food) do not require direct bank access. In general, card payments are still best for the majority of smaller, everyday purchases, while bank transfers are ideal for deliberate, high-value payments.

Physical retail also tends to be impractical for Pay by Bank, as customers can more easily pay in cash or swipe/tap their card at a physical POS.

Another common area for concern among businesses is PIS conversion. In B2C environments, especially, an extra redirection step to a banking interface can create friction and make some merchants hesitant to adopt Pay by Bank. However, in B2B use cases where payments are often invoice-based and higher value, PIS is already demonstrating stronger conversion rates. Payers are authenticated automatically, and businesses can rely on the payer’s intent to complete a transaction.

Additionally, as Pay by Bank is a European payment initiation service designed specifically for the SEPA area, it is not suitable for cross-border, non-SEPA transactions that are outside of that scope.

6. Are consumers already using Pay by Bank?

Across Europe, many consumers are already embracing Pay by Bank thanks to its convenience.

While card-based payments certainly still hold the crown in terms of popularity, it’s a smart business decision to start enabling new payment methods like Pay by Bank early. Instant payments and direct bank transfers are a growing focus among regulators in Europe and are likely to see a noteworthy uptick in usage over the coming decade.

7. Pay by Bank in Europe: Regulations and infrastructure

In Europe, Pay by Bank is built on a layered regulatory and infrastructure framework. At its foundation is the revised Payment Services Directive (PSD2), which introduced Open Banking and established the legal basis for Payment Initiation Services. PSD2 mandates Strong Customer Authentication (SCA) and requires banks to provide licensed third-party providers with secure API access to customer accounts.

Payments themselves are executed over SEPA credit transfer rails, standardized under the SEPA Regulation, which harmonizes euro transfers and direct debits across participating countries.

More recently, the Instant Payments Regulation (IPR) has further strengthened this infrastructure. IPR requires payment service providers offering euro credit transfers to also support instant euro transfers, ensuring funds can be received within seconds, 24/7. It also introduces fee parity requirements (instant transfers cannot cost more than standard transfers), adapted sanctions screening rules, and Verification of Payee (VOP) mechanisms to reduce fraud.

Together, PSD2, SEPA, and IPR create a regulatory environment that supports secure, real-time, and interoperable bank-to-bank payments across the euro area.

8. When does Pay by Bank make sense for your business?

Pay by Bank is a good option for businesses focused on improving the resilience of their payment operations. It works best as a strategic addition to cards and within your broader payment mix, and should be deployed where it makes the most economic and operational sense. Pay by Bank performs particularly well when you want to prioritize:

- Lowering payment processing costs

- Eliminating chargebacks

- Reducing fraud exposure through bank-level authentication

- Achieving faster settlement times and improved cash flow visibility

- Streamlining reconciliation with structured payment references

- Diversifying payment rails to reduce operational risks

- Offering a bank payment option without embedding payment accounts directly into your product

Moving payments between bank accounts with fewer intermediaries involved can significantly reduce per-transaction fees and largely remove the risk of chargebacks.

Pay by Bank extends across many payment use cases and can be equally effective for:

- Invoice and B2B payments

- Checkout interfaces

- Account top-ups and wallet funding

- Loan repayments

- Supplier and bulk payouts

- As a complement to recurring payments and subscription billing

The goal with Pay by Bank is typically not to replace cards altogether but rather to optimize your payment environment. Adding Pay by Bank where it fits best allows you to build a more cost-efficient and operationally resilient payment system.

9. The future of Pay by Bank

As the data confirms, Pay by Bank is ramping up in continental Europe.

At Powens, we offer the Open Banking capabilities you need to easily connect to and enable Pay by Bank as a payment method. Our Payments solution and Pay by Bank product allow real-time, account-to-account payments to be initiated on your website or via link or QR code. With our payment initiation services, you gain the ability to customize transaction labels and include specific payment references that automate reconciliation.

Whether you’re dealing with one-time payments or recurring billing cycles, Powens has solutions that can instantly enhance your payment experiences.